2022 marked the end of a 14 year old monetary policy experiment, during which the Federal Reserve (and other major central banks) generally held short term interest rates close to zero and printed money to buy long-term bonds in order to lower long-term interest rates. This experiment was initially an attempt to save the global financial system from collapse during the Great Financial Crisis of 2008. It then morphed into an attempt to support economic growth and financial markets, a shift from the Fed’s traditional mandate of supporting price stability and employment. Since the financial crisis, Wall Street pundits, ever lovers of acronyms, adopted the term TINA (There Is No Alternative), meaning that there is no alternative to buying stocks, given the paltry yields offered by bonds. This investment thesis was bolstered by the belief that stocks would not decline much given the plentiful cheap funds made available by Fed policy, which caused investors to ignore (or blithely accept) high valuations….a recipe for losses once the punch bowl was taken away.

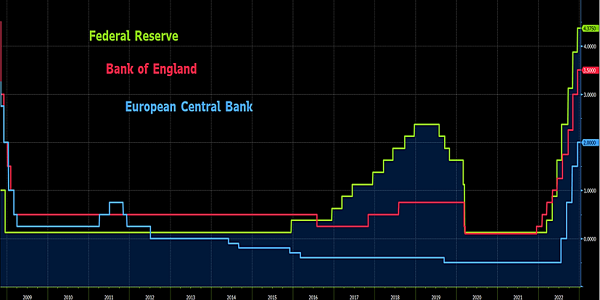

The Fed began raising interest rates in early 2022 in a belated attempt to combat elevated inflation. The Bank of England and the European Central Bank also began tightening monetary policy, albeit to a lesser degree. Graph 1 shows the rapid rises in short-term policy rates by three major central banks in 2022 compared to the years following the financial crisis.

Graph 1

Source: BBG

There was nowhere for investors to hide in 2022, as all major assets classes suffered significant losses. US and non-US stock markets lost 16- 18%, and high yield bonds returned -11%. Even high grade bonds, in recent decades a usually reliable portfolio hedge against declining equity markets, were down 13%.

Initially, stock and bond markets declined amid concerns that the Fed was late to counter price pressures; when (with its credibility at stake) the Fed finally started aggressively raising interest rates, investor sentiment began to shift from fear of inflation to fear that an overly aggressive Fed might send the economy into recession, perhaps a severe one. The steep losses in high grade bonds highlight the material price risk that SFA has been warning about for years.

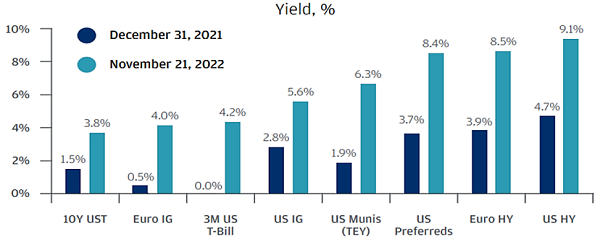

Despite the unpleasant experience of double-digit portfolio losses in 2022, it’s important to remember that market losses mean lower prices, and thus create opportunities for strong future returns. Therefore, astute investors must look forward to future opportunities, rather than looking back and extrapolating poor recent results into the future. Exactly such opportunities have emerged in fixed income markets, which have experienced a tectonic re-pricing of risk, and now represent a vastly better risk/reward proposition than a year ago. Graph 2 compares yields on various bond market sectors today to a year ago, and demonstrates that far higher yields are now available to investors. In other words, there now are alternatives to stocks, and in some cases compelling ones.

Graph 2

Source: JPM, BBG

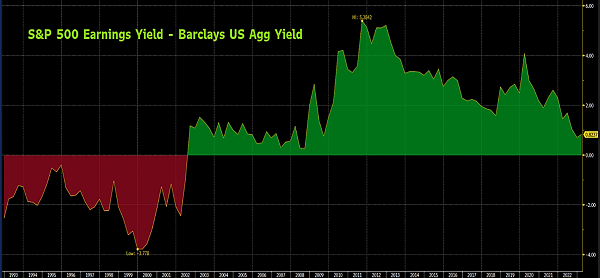

While bonds have re-priced over the last year, so have stocks: the US stock market price/earnings (P/E) ratio has fallen from an all-time high level to just slightly above the long-term average. So, while stocks are much cheaper than a year ago, they still are not cheap by historical standards. Additionally, they now must compete with bonds for investor cash. Given the re-pricing of both sectors, it makes sense to compare the relative attractiveness of stocks versus bonds. Graph 3 shows the US stock market earnings yield (earnings/price, or the reciprocal of the P/E ratio) minus the yield on the Barclays US Aggregate high grade bond index over a 29 year period. The differential is the lowest it has been in 15 years, meaning bonds are cheaper relative to stocks.

We don’t have a strong view on the short-term direction of markets: it’s certainly possible that inflation has peaked, the Fed stops tightening soon, and the economy avoids a recession in 2023. If these things occur, then probably both stocks and bonds will produce strong positive returns. However, if inflation accelerates again and the Fed continues aggressive hiking, and/or the economy slips into recession, then both sectors may do poorly. Or, if the Fed stops hiking soon but we nevertheless enter recession, then probably stocks will do poorly and bonds will do well in 2023. In any case, both sectors are far more attractively priced than a year ago, and bonds are probably the better relative value. We continue to discuss our sector allocations, and are inclined to add risk at lower levels (as we did last fall, when we added high yield bond exposure).

Graph 3

Source: BBG

Thank you for your trust, and please let us know if you have any questions, or would like to review your portfolio and the appropriateness of your investment strategy given the current market environment.

The information contained within this letter is strictly for information purposes and should in no way be construed as investment advice or recommendations. Investment recommendations are made only to clients of Santa Fe Advisors, LLC on an individual basis. The views expressed in this document are those of Santa Fe Advisors as of the date of this letter. Our views are subject to change at any time based upon market or other conditions and Santa Fe Advisors has no responsibility to update such views. This material is being furnished on a confidential basis, is not intended for public use or distribution, and is not to be reproduced or distributed to others without the prior consent of Santa Fe Advisors.

To Top

To Top