Every year there are headline economic and political events that define financial market moves for posterity. Every year there are also headlines reflecting expectations of events that move markets in the short run, but do not occur as predicted and are therefore largely forgotten by history. When such expectations are not realized, markets experience temporary volatility as they reprice assets to reflect a reality that differs from consensus forecasts.

This phenomenon occurred in both of the last two years, where consensus views were discredited during the year.

At the beginning of 2023, there was almost a universal consensus among Wall Street forecasters that there would be an economic recession that year. The forecasts differed only in the expected timing and severity of the recession. That consensus proved wrong and as the resilience of the economy became clear, the US stock market steadily moved higher. The result was a 26.3% return for the S&P 500 for the year.

At the beginning of 2024, there was a strong consensus that continued reductions in the rate of inflation would prompt the Federal Reserve to aggressively cut interest rates to support the economy – at that time the consensus was that the Fed would cut interest rates by 1.6% by year end. Although the Fed did in fact cut rates in 2024, the total cut was 1% – far less than expected by markets. Among the results was significant volatility in the high-grade bond market, with yields rising (and prices falling) as bonds adjusted to revised expectations, before a rally late in the year as the Fed began cutting rates. Stocks had another banner year, with the S&P 500 returning 25%, only the ninth time in history that the US stock market produced two consecutive years of 25%+ returns.

Now as 2025 begins, it is worthwhile for us to examine what consensus expectations are for the coming year, particularly to assess whether that any aggregate forecasts appear unduly optimistic or pessimistic.

The US economy is strong and is expected to stay so, with expectations of 2.5%-3% growth for the year. Core inflation, currently at 2.7%, is expected to continue to moderate. The Federal Reserve is expected to make modest further rate cuts (0.4% as of this writing). Company earnings are expected to remain robust, rising by about 10%, with corresponding stock market return forecasts also centered around 10%.

While none of these forecasts seem to be unreasonable, there are of course always risks.

Risks

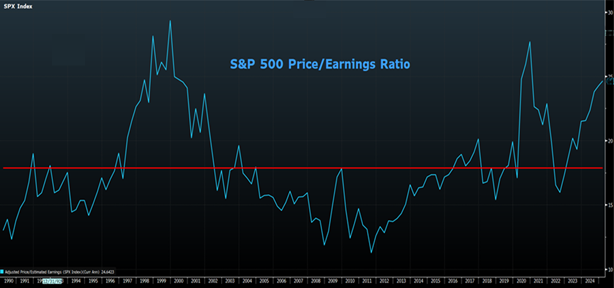

One glaring risk is the elevated valuation of our stock market. Graph 1 shows the price/earnings ratio of the S&P 500, which currently trades at 25x the previous year’s earnings.

Graph 1

Source: BBG

This valuation level is about 40% higher than the long-term average, and has been exceeded only twice in history: before the 2000 dot com crash, and in 2021. As we have often noted, stock valuations are poor predictors of short-term market moves, so the fact that equities are so expensive does not necessarily mean that they are likely to decline any time soon. High valuations do, however, make the market more vulnerable to negative surprises. Nevertheless, if company earnings meet expectations, current extended valuations are likely to be sustained, in which case the market would likely rise along with earnings.

There are both opportunities and risks posed by the change in policies that the new Trump administration will implement. A more friendly business regulatory environment and lower taxes are strong tailwinds for the market, while threatened tariffs, if implemented as advertised, represent headwinds to growth and would be inflationary.

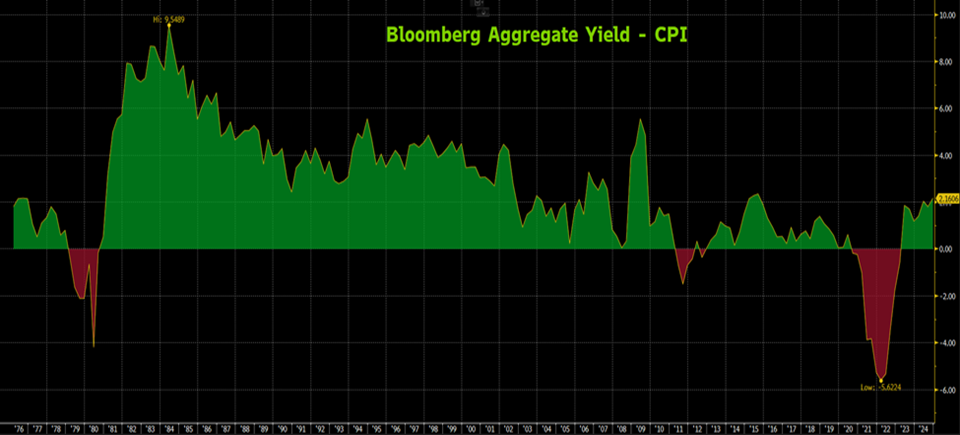

After years of offering anemic yields following the Great Financial Crisis, the bond market now offers reasonably attractive yields. Graph 2 shows the real yield provided by the Bloomberg Aggregate high-grade bond index. The real yield is the index yield minus inflation. As the graph shows, the market now offers real yields as high as they have been in 15 years. This means not only that investors stand to reap attractive returns from bonds, but also suggests that bonds are likely to be a portfolio hedge against stock market declines, with higher yields likely to attract investors and generate positive returns if stocks decline. Additionally, with expectations for only modest Fed rate cuts in 2025, there is less room for a downside policy disappointment.

Graph 2

Source: BBG

Household Outlook

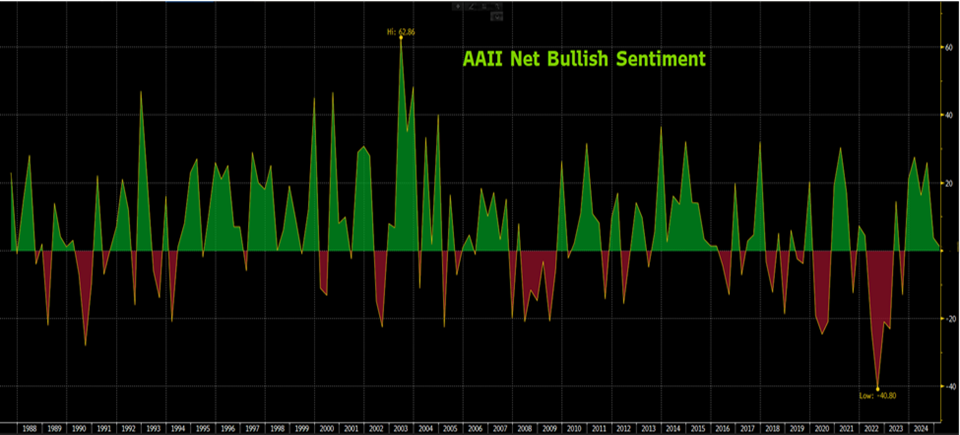

As we examine consensus forecasts in assessing the 2025 investment landscape, we should also look at household views, from which we can also glean important information. Graph 3 shows the net bullishness of individual retail investors (the % of investors with a bullish outlook minus the % of investors with a bearish outlook). Individual investors in aggregate tend to be reliable contra-indicators: when a significant excess of investors are bullish, the market tends to go down, and when retail investors are overwhelmingly bearish, the market tends to go up. Currently, bullish and bearish views are about equal among retail investors, indicating an absence of concerning bullishness. Practically, this means that there is ample room for increased bullishness, and therefore increased potential buying of stocks.

Graph 3

Source: BBG

Graph 4 shows household consumer sentiment on the overall economy and household finances. Again, this is a contra-indicator. As the graph illustrates, over the past 50 years, when household confidence has hit a cyclical low, the average stock market return for the next 12 months has been 24.1%. Conversely, when sentiment has hit cyclical peaks, the average forward 12-month return has been a paltry 3.5%. Currently, household sentiment is below the long-term average, which augurs well for 2025 market returns.

Graph 4

Source: JPM, FactSet, S&P, U Michigan

As always, there are reasons to be either bullish or bearish. The biggest market risks tend to be those that few are thinking about. The impact of unexpected events is particularly large because such occurrences are not reflected in current market prices. As we step back and assess the 2025 environment, it is also important to be mindful that historically the US stock market has risen in about 75% of years.

All considered, we believe that the right approach as we enter the new year is to stay close to neutral relative to our portfolio risk targets and portfolio risk according to individual client situations and objectives. Thank you for your trust, and please contact us if you have any questions, or would like to review the appropriateness of your portfolio risk.

The information contained within this letter is strictly for information purposes and should in no way be construed as investment advice or recommendations. Investment recommendations are made only to clients of Santa Fe Advisors, LLC on an individual basis. The views expressed in this document are those of Santa Fe Advisors as of the date of this letter. Our views are subject to change at any time based upon market or other conditions and Santa Fe Advisors has no responsibility to update such views. This material is being furnished on a confidential basis, is not intended for public use or distribution, and is not to be reproduced or distributed to others without the prior consent of Santa Fe Advisors.

To Top

To Top