They finally did it. On September 18, in a move that had been anticipated for almost a year, the Federal Reserve Bank finally cut short term interest rates (by half a percent). This move followed a steady decline in inflation, and a year of significant interest rate volatility, as large changes in market expectations of the size of pending rate cuts were reflected in bond market yields and prices. While expressing confidence in the economy and noting that inflation remains above their 2% target, Fed Governors signaled that several more rate cuts are anticipated; both the Fed forward guidance and current market expectations point to another 1% of rate cuts over the next four months, and close to 2% more in cuts by the middle of 2026. Clearly, the Fed believes that the balance of risks has shifted from price pressures to economic growth.

Market reactions to the Fed move have been modest, reflecting the fact that the move was widely anticipated. The S&P 500 initially rallied and set several new all-time highs, but has been largely flat since. While short term interest rates fell, longer maturity interest rates have actually slightly risen since the rate cut, likely reflecting both confidence in the economy as well as some concern that the Fed may be backing away from the inflation fight prematurely.

As investors, this leaves us in a very familiar situation – there is clearly evidence to support both bullish and bearish arguments for both the stock and bond markets.

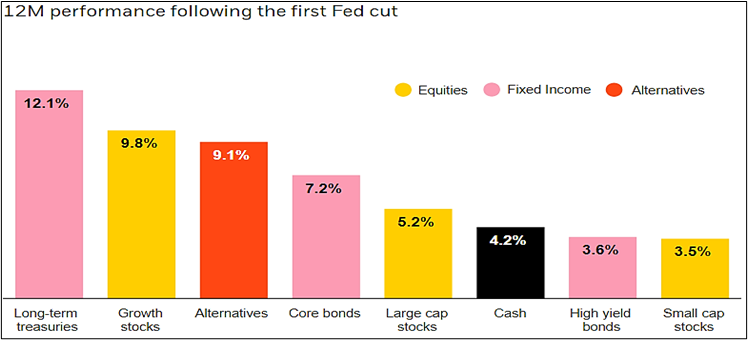

The bullish case is probably best summed up in the old Wall Street truism: Don’t Fight the Fed. When the Fed embarks upon an easing cycle, rate cuts tend to continue for several quarters, during which both stocks and bonds have historically tended to perform quite well. Graph 1 shows the average 12 month performance of various asset classes following the first Fed rate cut in easing cycles since 1981, demonstrating that these asset classes tend to be propelled by the tailwind of lower rates. Stocks benefit as companies get lower financing costs, and bond prices rise as interest rates drop. We would be unwise to lightly dismiss such a powerful historical precedent. Recent company earnings growth has been robust; should that continue, stocks will likely continue to rise, despite their currently lofty valuations.

Chart 1

Source: BlackRock, Morningstar

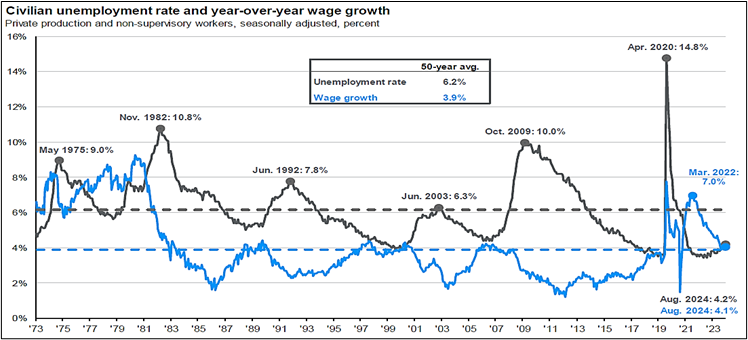

As always, there is also a bearish case to be made, which we would be equally remiss not to consider. Whereas the economy remains strong, there has been signs of softening in manufacturing and also in the labor market. Graph 2 shows a decline in US wage growth, as well as an uptick in unemployment (though both remain at healthy levels).

Chart 2

Source: J.P. Morgan Asset Management

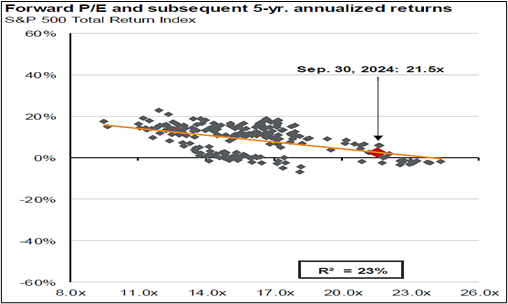

It is also possible that the Fed has prematurely declared victory against inflation, and that price pressures may re-emerge. The fact that longer term interest rates have risen slightly since the Fed cut short term rates suggests some concern about this risk in the bond market, as does the continued rally in gold prices. Finally, although high grade bonds now offer positive real yields (and are therefore arguably attractive), stock valuations (at least in the US) are quite expensive by historical measures. Graph 3 plots historical stock valuations against subsequent 5 year annualized returns, and suggests that investors might expect very muted equity returns for the next several years if historical relationships hold. Having said that, earnings will be key – if earnings growth remains strong, stocks are likely to continue to perform well.

Chart 3

Source: JPM, FactSet, Refinitiv Datastream, S&P, Thomson Reuters

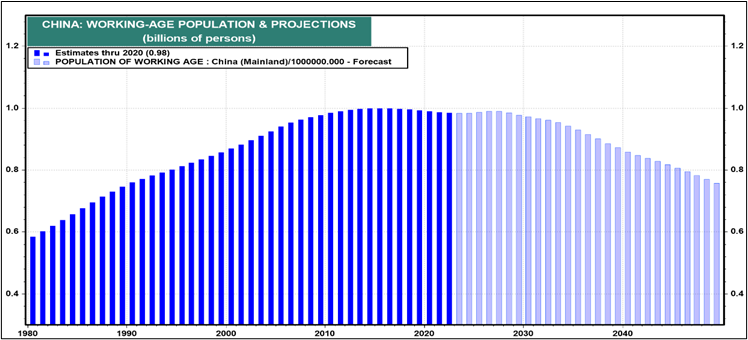

Finally, we should note that all the focus on the Fed’s turn toward monetary easing has diverted attention from a far larger package of both monetary and fiscal stimulus announced by the Chinese government a few days earlier. These measures are another effort to battle the economic stagnation that has plagued that country for years, particularly in the real estate sector. As a result of this stimulus (with more apparently forthcoming), various Chinese stock markets have skyrocketed, rallying by 25-30% in just three weeks. Whereas stimulus of this sort does tend to have a positive short term market impact (which will likely spill over into other Emerging Market economies and markets), it will not address the long-term fundamental problems that China has, including a command economy and a demographic time-bomb in the form of a rapidly aging and shrinking population. Graph 4 shows long term projections of the Chinese population, which is expected to plummet in coming decades, leading to a situation with too few workers supporting too many retirees. Just as the US debt is a major long-term problem for investors, so is this reality in the world’s second largest economy (which is the largest on a purchasing power adjusted basis).

Chart 4

Source: Yardeni, LSEG Datastream, Oxford Economics

In closing, whereas prevailing market events, valuations, and risks are always different, one thing is a constant: the future is uncertain, and both upside and downside risks exist. Given current risks and opportunities, we are maintaining exposures in our portfolios close to our neutral strategic positions, and are content to remain there until we see compelling dislocations.

Thank you for your trust, and please contact a SFA team member with any questions.

The information contained within this letter is strictly for information purposes and should in no way be construed as investment advice or recommendations. Investment recommendations are made only to clients of Santa Fe Advisors, LLC on an individual basis. The views expressed in this document are those of Santa Fe Advisors as of the date of this letter. Our views are subject to change at any time based upon market or other conditions and Santa Fe Advisors has no responsibility to update such views. This material is being furnished on a confidential basis, is not intended for public use or distribution, and is not to be reproduced or distributed to others without the prior consent of Santa Fe Advisors.

To Top

To Top